Introduction

Major banks have moved fast on AI agents. BNY now runs over 100 digital employees handling legal document review and operational workflows, cutting contract review time by 75%—from four hours to one hour across 3,000+ annual vendor agreements. JPMorgan's GenAI toolkit reaches 200,000+ employee desktops. Citi has deployed enterprise AI tools to roughly 150,000 colleagues.

None of this deployment has outrun the regulators by accident. Not one regulatory framework currently governs what happens when an AI agent causes a compliance failure.

Every layer of the existing compliance stack—KYC, AML, the Bank Secrecy Act—was written for human actors. An AI agent making autonomous decisions doesn't satisfy the identity, intent, or accountability requirements built into those frameworks. Banks are improvising to fill the gap, and that patchwork carries real legal exposure. This article breaks down where the regulatory frameworks fall short, how leading banks are responding, and what a defensible compliance posture for agentic AI actually looks like.

Key Takeaways

- Current KYC, AML, and BSA rules assume human identity and intent—AI agents don't naturally satisfy those requirements

- When an AI agent causes a compliance failure, liability remains legally ambiguous at most institutions

- AI agents introduce novel attack vectors that traditional security tools weren't built to detect

- Banks are filling the regulatory gap with internal policies, not settled law

- Compliant deployments require tamper-evident audit trails, scope enforcement, and defined human escalation paths

The Compliance Framework Gap: Why Existing Rules Don't Fit AI Agents

The Identity Problem

The BSA's definitional structure in 31 CFR 1010.100 defines "person" to include individuals and legal entities. It defines "financial institution" by listed institution types—banks, broker-dealers, money services businesses. An AI agent appears nowhere in those definitions.

When BNY issues login credentials to AI agents, or when an agent reviews a Suspicious Activity Report and routes it for filing, there is no regulatory definition of what that agent "is" in the eyes of regulators. Not a person. Not a legal entity. Not a system of record under any existing framework.

31 CFR 1020.220 requires Customer Identification Programs to contain risk-based procedures for verifying the identity of each customer. AML rules presume human intent behind suspicious activity patterns. The BSA demands a verifiable identity behind every reportable action. Autonomous agents satisfy none of these conditions without purpose-built governance overlaid on existing frameworks.

Why Model Risk Management Falls Short

SR 11-7—the Federal Reserve's foundational model risk management guidance—defines a model as "a quantitative method, system, or approach that applies statistical, economic, financial, or mathematical theories to process input data into quantitative estimates."

That definition fits a credit scoring model. It does not fit an AI agent that plans multi-step actions, calls external tools, and makes decisions across contexts it has never seen before.

Fed Governor Barr acknowledged this directly in an April 2025 speech, explicitly discussing "Gen AI agents" in banking and calling for governance review and updates to existing standards like SR 11-7—but stopping short of announcing a dedicated agent-specific framework.

The Accountability Vacuum

Existing frameworks place compliance accountability on humans: the compliance officer, the institution. When an agent acts autonomously and causes a violation, the accountability chain fractures. Three questions emerge that no current regulation answers cleanly:

- Is liability with the deploying bank that authorized the agent?

- Does it fall on the AI vendor whose model drove the decision?

- Or on the human manager the agent nominally "reports to"?

Cross-border deployments compound this further. An agent executing a transaction touching the EU, UK, and US simultaneously must satisfy conflicting regulatory requirements — with no single governance framework capable of resolving the conflict. Until regulators define the agent's legal standing, every autonomous action carries unresolved liability exposure.

Key Regulatory Challenges Banks Face When Deploying AI Agents

AML and Transaction Monitoring

AI agents can detect suspicious transaction patterns effectively. The compliance problem emerges when they act on those detections autonomously: flagging, blocking, or escalating without documented human intent.

31 CFR 1020.320 places SAR filing obligations on the bank and requires supporting documentation. The FFIEC SAR examination manual directs examiners to assess documentation of decisions, including decisions not to file. An AI agent that drafts or routes a SAR creates an audit artifact, but if the agent's reasoning isn't auditable and explainable, that SAR may not survive regulatory scrutiny.

Recent enforcement actions illustrate the stakes:

- OCC (2024): Consent order against TD Bank cited inadequate documentation of automated alert backlogs

- FinCEN (2018): Assessment found U.S. Bank had insufficient staffing to manage suspicious activity alerts from its automated monitoring systems

Neither case involved AI agents specifically. Both underscore that regulators expect human-reviewable documentation behind every automated compliance output.

KYC and Customer Due Diligence

FinCEN's CDD Final Rule requires covered financial institutions to establish written procedures for identifying and verifying beneficial owners of legal entity customers. When an AI agent conducts due diligenceby querying databases, cross-referencing sanctions lists, and generating risk scores, the process must still produce a defensible, human-reviewable decision record.

Most current agentic deployments cannot produce that record. For high-risk customers requiring Enhanced Due Diligence, the gap is sharper. FFIEC guidance expects documented, risk-based assessments, and an agent that cannot explain its risk determination in plain language creates direct audit exposure. Regulators cannot evaluate what they cannot read.

Data Privacy and Cross-System Access

AI agents processing compliance data ingest transaction records, CRM data, employee files, and external feeds. Each new data flow may not be covered by existing consent frameworks or privacy agreements.

GDPR Article 22 is directly relevant: data subjects have the right not to be subject to decisions based solely on automated processing that produce legal or similarly significant effects. The CJEU has held that credit scoring can fall under Article 22 where the score plays a determining role in a lender's decision. Banks running AI agents on customer financial data need to map each new agent integration against these obligations, not assume prior consent frameworks cover novel data flows.

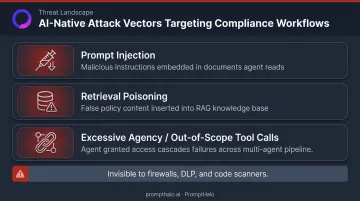

AI-Native Security Risks Inside Compliance Workflows

Legacy security tools—firewalls, DLP, code scanners—were designed for a world where threats arrive as malicious code or unauthorized network traffic. AI agents introduce a different attack surface: the data the agent reads can be the attack.

Prompt Injection

OWASP classifies prompt injection as the top LLM risk: user prompts or retrieved content alters LLM behavior in unintended ways. In a compliance context, an adversary can embed instructions inside documents the agent is reviewing—such as:

- A transaction memo flagged for review

- A vendor contract submitted for onboarding

- A customer email routed through a compliance queue

The agent then executes those instructions—clearing a flagged transaction, suppressing a SAR, or routing sensitive data to an unauthorized tool call—without any human ever seeing the manipulation.

Firewalls don't inspect inference-time content, and code scanners don't read documents. This class of attack is invisible to the existing security stack.

Retrieval Poisoning

RAG-based compliance agents retrieve context from internal knowledge bases: policy documents, regulatory guidance, customer histories. If an adversary poisons the retrieval index—inserting false regulatory context or altered policy documents—the agent may retrieve that content and act on it, approving non-compliant actions it believes are sanctioned.

NIST AI 600-1 (July 2024) identifies data and retrieval poisoning as primary GenAI risks. OWASP's 2025 list covers vector and embedding weaknesses as well.

Out-of-Scope Tool and API Calls

OWASP LLM06 addresses excessive agency: LLM systems granted access to functions, tools, or APIs can take damaging actions if their authority isn't scoped and enforced. In multi-agent compliance pipelines—where one agent hands off to another, which calls a database, which triggers a transaction—one compromised agent can cascade failures across the entire workflow.

Without per-action scope enforcement, the blast radius of a single manipulation extends across every downstream agent in the pipeline.

How PromptHalo Addresses This Attack Surface

Each of these risks shares a common trait: they exploit the gap between what an agent is authorized to do and what it actually does at runtime. PromptHalo was built to close that gap. The platform sits inline on every inference, tool call, and agent-to-agent handoff, making an allow/restrict/challenge/deny/monitor decision in under 100ms—before any action executes.

Key capabilities relevant to banking compliance workflows:

- Injection detection: embedding-based scoring against a continuously updated Threat Library catches both direct prompt injection and RAG retrieval manipulation

- Tool call enforcement: Unsafe Tool Actions Prevention enforces authority per action externally—an agent cannot grant itself more access than it was assigned

- Security passports with authority decay: permissions diminish over time and steps, forcing re-authorization when thresholds are exceeded

- Behavioral drift detection: session-over-session output tracking surfaces gradual shifts that indicate compromise or model degradation before they become incidents

The platform deploys across any AI application from any vendor without touching underlying models—no retraining, no code rewrite, operational in under a day. For banks with heterogeneous AI stacks across multiple vendors, that model-agnostic architecture cuts deployment complexity significantly.

How Banks Are Navigating the Compliance Gap Today

Without formal regulatory guidance, banks are improvising through three strategies:

Persistent agent identities — Assigning AI agents credentials with defined access permissions and human manager accountability chains, similar to how contractors are credentialed. BNY's "digital employees" model, with named supervisors and personas, exemplifies this approach.

Internal liability policies — Treating AI agent actions as extensions of the human supervisor's accountability, so the compliance officer "owns" whatever the agent does.

Escalation protocols — Routing AI-generated outputs to human compliance officers before any regulatory action is taken—no agent-filed SARs, no agent-approved EDD without human sign-off.

These approaches are reasonable given the absence of formal guidance. They're also legally fragile. If a regulator challenges an AI-generated SAR or an agent-adjudicated KYC record, an internally developed governance policy may not constitute a defensible compliance control. The CFPB and federal partners stated clearly in 2023 that automated systems are not an excuse for lawbreaking behavior.

That fragility matters because regulatory signals are converging on formalization. The EU AI Act's Article 6(2) and Annex III classify AI systems used for creditworthiness assessment and credit scoring as high-risk, requiring conformity assessments and documentation. OCC Acting Comptroller Hood's April 2025 remarks identified transparency, accountability, fairness, and model risk as AI governance priorities.

The formal framework hasn't landed yet — but the trajectory is no longer ambiguous.

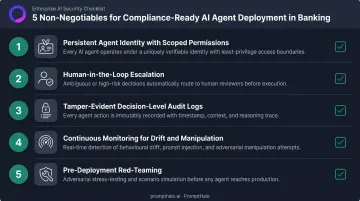

What a Compliance-Ready AI Agent Deployment Looks Like

Based on existing MRM guidance, BSA/AML requirements, and emerging regulatory signals, five elements are non-negotiable:

Persistent agent identity with scoped permissions — Each agent needs documented authority limits, defined access scope, and a named human accountable for its actions.

Human-in-the-loop escalation — Any action touching SAR filing, EDD approval, or high-risk transaction decisions requires human review before execution. The agent prepares; the human decides.

Tamper-evident, decision-level audit logs — Logs must record agent reasoning, data accessed, tools called, and outcomes at each step. Append-only, replayable, and mapped to established frameworks.

Continuous monitoring for drift and manipulation — Behavioral changes, out-of-scope actions, and adversarial manipulation must be detected in real time, not discovered in a post-incident review.

Pre-deployment red-teaming — Before any agent goes live in a regulated workflow, it needs adversarial testing across its full attack surface: prompt injection probes, retrieval poisoning attempts, multi-step adversarial task chains.

Of these five elements, the audit trail draws the most direct regulatory scrutiny. It's the one examiners will ask to see first.

The Audit Trail as the Linchpin

Without replayable, explainable agent decision logs, a bank cannot demonstrate that its AI-assisted compliance decisions were sound. Three existing requirements make this concrete:

- SR 11-7 requires model documentation and validation for any model influencing risk decisions

- 31 CFR 1020.320 requires SAR supporting documentation with a clear evidentiary basis

- CFPB adverse-action rules require specific reasons for credit decisions even when complex algorithms are used

PromptHalo's audit logs capture every decision with the reason, the acting agent or passport identity, session and tenant context, and a timestamp. Logs are append-only and tamper-evident, structured for compliance export and regulatory review — built into the enforcement layer, not added as a reporting afterthought.

Institutions that build this runtime governance infrastructure now (before formal regulation arrives) will enter the examination process with documented compliance posture and an operational track record. When regulators finalize requirements, that history is evidence, not just intention.

Frequently Asked Questions

Do current KYC and AML regulations apply to AI agents in banking?

Current KYC and AML rules were written assuming human actors, so AI agents don't naturally satisfy requirements for identity verification or documented human intent. Banks must build additional governance layers—persistent agent identities, escalation protocols, explainable audit trails—to bridge the gap between what regulations require and what agents currently provide.

Who is liable when an AI agent causes a compliance failure at a bank?

Liability currently defaults to the deploying institution under existing frameworks, but the legal chain becomes ambiguous when multiple vendors and systems are involved. Most banks are navigating this through internal policy rather than settled law — leaving real exposure if a regulator challenges an AI-generated compliance decision.

What is the difference between AI agents for compliance and AI agents that must themselves be compliant?

AI agents for compliance are tools that help banks meet regulatory obligations—AML monitoring, KYC screening, SAR drafting. AI agents that must be compliant means ensuring those autonomous agents themselves operate within regulatory boundaries. Both challenges coexist: an agent can detect financial crime while simultaneously creating regulatory exposure through unauditable decision-making.

What audit trail requirements apply to AI agent decisions in banking?

No AI-specific audit trail standard is finalized in the US, but SR 11-7 model risk guidance and AML recordkeeping rules require automated compliance decisions to be documented, explainable, and reproducible. In practice, that means decision-level logs capturing reasoning, data accessed, tools called, and outcomes.

How does the EU AI Act affect US banks deploying AI agents?

The EU AI Act classifies AI systems for natural-person creditworthiness assessment and credit scoring as high-risk under Annex III, requiring conformity assessments and audit documentation. US banks with EU operations or EU customer data may need to comply. Even without direct EU exposure, the Act is raising the documentation bar that US regulators are increasingly likely to reference.