Introduction

Financial institutions process billions of transactions daily — and that scale makes them a target unlike any other. According to the IMF, cyberattacks against the financial sector have nearly doubled since the pre-pandemic period, with banks consistently the most frequent targets.

The problem isn't just volume. Modern attacks — synthetic identity fraud and real-time payment manipulation — move faster than human analysts or legacy systems can respond. A rule that takes days to write and deploy offers little protection against a fraud pattern that evolves overnight.

Banking security teams face a compounding bind: exploding attack volumes, detection windows measured in seconds, and regulators demanding full auditability of every AI-driven decision. Rule-based tools weren't designed for any of that.

This article examines how machine learning is reshaping real-time threat detection in banking — from payment fraud and insider threats to AI-native attacks targeting agentic systems that traditional fraud models weren't built to see.

Key Takeaways

- ML models detect novel threats in real time by learning behavioral patterns — not just matching pre-coded rules

- Account takeover losses reached nearly $16B in 2024, making behavioral analytics a critical priority

- Agentic banking systems expose a new attack surface — prompt injection, retrieval poisoning, and AI-targeted jailbreaks

- Regulatory frameworks (FFIEC, NIST AI RMF, EU AI Act) increasingly require explainable, auditable AI decisions

- Effective deployment requires continuous retraining, explainable outputs, and workflow integration

The Evolving Cyber Threat Landscape in Banking

Banking threats have shifted from opportunistic to orchestrated. Credential stuffing and basic phishing still exist, but they now share the threat landscape with synthetic identity fraud, mule account networks, and automated account takeover campaigns running at industrial scale.

The Federal Reserve's 2024 FI Risk Officer Survey documents the scope: fraud attempts rose 10% for checks, 9% for ACH, and 6% for debit cards. Mule account activity — a marker of organized fraud networks — increased 12% as a notable concern, with 18% of financial institutions reporting pronounced pressure.

The Federal Reserve Payments Improvement program identified synthetic identity fraud as the fastest-growing financial crime in the U.S., with losses running into the billions annually. These aren't amateur operations — they're coordinated campaigns exploiting gaps between payment rails, identity systems, and fraud detection tools.

That sophistication is now extending into a new vector: the AI systems banks have deployed to fight fraud are themselves becoming targets.

The Newest Threat Layer: AI-Powered Attacks

Banks are deploying AI agents for customer service, loan origination, compliance screening, and payment processing. That creates an attack surface that didn't exist five years ago.

Adversaries have begun targeting those agents directly through:

- Prompt injection — embedding malicious instructions in user inputs to hijack agent behavior

- Retrieval poisoning — corrupting the data sources an agent draws from

- Jailbreaks — overriding the constraints built into an agent's instructions

- Excessive agency — manipulating an agent into executing actions beyond its intended scope

FS-ISAC projects that U.S. losses from deepfake and AI-generated fraud could reach $40B by 2027. The threat isn't hypothetical — it's a risk class that's actively being cataloged by OWASP and documented by financial sector information-sharing bodies.

Why Traditional Security Systems Struggle to Keep Up

Rule-based and signature-based detection systems share a fundamental limitation: they only catch threats they've already seen. Any novel fraud pattern, zero-day exploit, or manipulation of an AI agent bypasses them entirely. You can't write a rule for something you haven't encountered yet.

Speed compounds the problem. FedNow's operating procedures allow a response window of 1 to 5 seconds for instant payments — and once a payment settles, it's final. Fraud detection that operates on batch processing or post-transaction review offers essentially no protection in this environment.

Then there's the catch-rate reality. Gartner's 2026 bank payments fraud benchmark found that over one-third of banks detect fewer than 60% of fraudulent transactions before losses occur. Only 31% achieve preemptive detection above 80%. Those aren't acceptable numbers when payments are irrevocable.

The Specific Gaps That Put Banks at Risk

Those detection failures aren't random — they trace back to predictable structural weaknesses in how legacy tools were built:

Behavioral blind spots — Rule-based systems can't detect anomalies that don't match known patterns. An employee downloading unusual volumes of customer data at 2 a.m. on a Friday doesn't trigger a rule if no one wrote that rule.

No visibility into AI-layer actions — Firewalls, DLP tools, and code scanners were designed for network perimeters and file-level threats. They have no instrumentation for monitoring autonomous AI decisions, tool calls, or agent-to-agent handoffs inside modern banking workflows.

Audit trail deficiencies — Modern regulators expect banks to demonstrate that AI systems are auditable and controllable. Legacy tools weren't built to produce the decision-level, interpretable records that satisfy current AI governance requirements.

Alert fatigue — A peer-reviewed study on bank anti-fraud systems found that only 1 in 5 blocked payment transactions was actually fraudulent, and every 6th user was mistakenly flagged over the course of a year. That volume of noise buries real threats and degrades analyst effectiveness over time.

How Machine Learning Powers Real-Time Threat Detection

The foundational difference between ML and rule-based systems is learning. ML models analyze historical data to recognize patterns (both known fraud signatures and subtle behavioral deviations) and they update as new data flows in. That means they can flag novel threats in real time, not just threats that fit pre-existing categories.

Core ML Techniques Used in Banking Security

Supervised learning trains on labeled datasets of fraudulent versus legitimate transactions. Given enough historical data, models like gradient boosting and neural networks can classify new activity with high confidence — recognizing combinations of features (transaction amount, geolocation, device fingerprint, time-of-day, velocity) that together signal fraud even when no single factor is conclusive.

Unsupervised learning and anomaly detection don't require labeled data. Instead, they establish behavioral baselines for users, accounts, and systems, then flag statistical outliers. A corporate account initiating hundreds of micro-transfers, or an employee downloading large volumes of customer records outside normal hours — neither requires a pre-written rule to detect.

Deep learning and neural networks, particularly LSTMs and recurrent architectures, excel at sequential data. Banking activity is inherently sequential: transaction histories, session behavior, multi-step authentication flows.

These models can identify multi-step fraud chains where no single event looks suspicious but the sequence is anomalous — catching patterns that simpler models miss entirely.

NLP handles unstructured data across several threat surfaces:

- Phishing email detection and social engineering in customer communications

- Adversarial instructions embedded in text inputs targeting LLM-powered banking systems

- Prompt injection attacks directed at AI agents operating within financial workflows

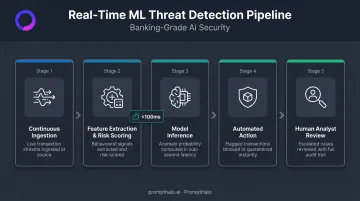

The Real-Time Detection Pipeline

Understanding these model types clarifies how they work together in practice. A functioning ML threat detection pipeline in banking operates as follows:

- Continuous ingestion of transaction logs, user sessions, and API calls in real time

- Feature extraction and risk scoring applied to each event as it arrives

- Model inference at sub-second speed, producing a risk verdict per event

- Automated action — block, challenge, flag, or allow — executed before the transaction settles

- Human analyst review of escalated cases, with explainable AI output that shows which signals triggered the flag

That last step matters as much as the first. ML models that produce black-box alerts don't help analysts, and they don't satisfy regulators either. Explainability isn't optional.

Key ML Applications for Banking Security

Transaction Fraud and Payment Anomaly Detection

ML models can score every transaction against behavioral baselines and historical fraud patterns in real time. Ensemble models combine multiple signals — transaction amount, geolocation, device fingerprint, time-of-day, peer group behavior — to identify fraudulent activity before the transaction settles.

Swift's AI-enhanced fraud detection service, launched in January 2025, illustrates how this works at scale: the system uses pseudonymized data from billions of annual Swift-network transactions to flag suspicious activity in real time, operating across the network rather than within a single institution's data silo.

Account Takeover and Identity Fraud

Javelin reported that account takeover victims lost nearly $16B in 2024, up $2.9B from the prior year. Checking accounts were the primary target, with 39% of ATO victims reporting checking-account compromise.

ML detects ATO by identifying behavioral anomalies across the full session — not just at login. Common indicators include:

- Rapid contact-detail changes immediately followed by a funds transfer

- Authentication from an unrecognized device in an unusual location

- Session behavior inconsistent with the account's historical patterns

User and Entity Behavior Analytics (UEBA) builds continuous risk profiles for each account, so deviations stand out against an established individual baseline rather than a generic threshold.

Insider Threat Detection

Verizon's 2024 DBIR found that internal actors were responsible for 31% of financial-sector breaches — a meaningful share given the privileged access bank employees have to sensitive customer and financial data.

Unsupervised ML is particularly well-suited to insider threat detection because insider attacks often have no historical precedent to match against. Instead, the model learns what normal looks like for each employee or contractor — typical access patterns, data volumes, working hours — and flags deviations. Early warning signals include:

- Bulk customer data downloads outside normal volume thresholds

- After-hours database queries with no business justification

- Access to systems outside an employee's established scope

All of these can surface before a breach completes.

Detecting AI-Native Threats in Agentic Banking Systems

Conventional fraud models weren't built for agentic AI — and attackers know it. As banks deploy AI agents for customer interactions, compliance screening, loan origination, and payment workflows, those agents become targets.

The OWASP LLM Top 10 catalogs the specific risks: prompt injection, sensitive information disclosure, data and model poisoning, excessive agency, and supply-chain weaknesses. FS-ISAC has explicitly identified AI as exposing financial firms to new vectors of cyberattack, fraud, and misuse.

Detecting these threats requires ML operating at the inference layer — monitoring every agent decision, tool call, and model output in real time. This differs from transaction-layer fraud detection, which monitors payment events. An agent executing an unauthorized API call, a retrieval-poisoned knowledge base feeding corrupted data into a compliance workflow, a jailbroken customer service agent disclosing account information it shouldn't — none of these show up in a transaction log.

PromptHalo's runtime enforcement engine operates inline at this layer, evaluating each agent action — tool calls, model outputs, and agent-to-agent handoffs — in under 100ms. The system can allow, restrict, challenge, deny, or monitor each action before it executes, without requiring model retraining or code rewrites. For banks deploying agentic AI, this means the AI layer gets the same level of real-time security scrutiny as the transaction layer.

Implementation Considerations for Banking Security Teams

Deploying ML threat detection effectively requires more than selecting a model. Three prerequisites determine whether a deployment succeeds or stalls:

- Training data quality — Models trained on incomplete or unrepresentative data underperform. Banks need diverse historical data: transaction records, fraud labels, behavioral logs across user populations and payment rails.

- Infrastructure integration — ML systems need to connect to existing data flows (transaction systems, API gateways, authentication logs) to operate in real time. Integration gaps create detection blind spots.

- Escalation workflows — Automated ML responses need clear handoffs to human analysts. What gets blocked automatically? What gets flagged for review? How fast does a reviewer need to act?

Model governance is an ongoing challenge that many teams underestimate. ML models trained on historical patterns degrade as threats evolve and as the bank's own transaction patterns shift — seasonal volume changes, new product launches, regulatory changes affecting payment flows.

Static models lose accuracy over time. Continuous learning pipelines and regular performance monitoring aren't optional maintenance; they're essential to keeping detection rates from eroding.

Detection rates aren't the only metric at risk. Explainability failures expose banks to a separate problem: black-box alerts slow analyst investigations and draw regulatory scrutiny. ML-driven security tools need to produce decision-level outputs that show why something was flagged, not just that it was.

For banks deploying AI agents alongside traditional ML fraud controls, this explainability requirement extends to every autonomous action those agents take. PromptHalo's enforcement layer addresses this at the agent level: every decision produces a signed, tamper-evident audit log entry capturing the decision, its reason, the acting agent's identity, session context, and timestamp. Those logs map to OWASP LLM Top 10, NIST AI RMF, and the EU AI Act — giving compliance teams replayable decision trails that hold up under examination.

Regulatory Compliance and AI Governance in Banking

Regulators have been watching AI adoption in banking closely, and the expectations are becoming more specific.

Key frameworks and requirements:

| Framework | Scope | Key Requirements |

|---|---|---|

| FFIEC IT Handbook (2021) | U.S. banks | AI/ML explainability, bias testing, monitoring, independent validation |

| OCC Bulletin 2011-12 / SR 11-7 | Model risk management | Model governance, validation, back-testing, documentation |

| OCC Bulletin 2026-13 | Revised MRM guidance | Risk-based approach; explicitly excludes generative and agentic AI (still novel) |

| NIST AI RMF 1.0 | Voluntary AI governance | Govern, Map, Measure, Manage functions for AI risk |

| EU AI Act (2024/1689) | EU operations | High-risk classification for creditworthiness AI; documentation, logging, human oversight required |

The 2026 revised model risk guidance from OCC, the Fed, and FDIC explicitly excludes generative and agentic AI from scope — regulators consider them too novel for the existing framework. That exclusion creates a governance gap, not permission to proceed without controls. Banks deploying agentic AI need AI-specific governance overlays that traditional model risk management doesn't currently address.

The Citibank enforcement precedent is instructive even without an AI-specific case: the OCC assessed a $400M civil money penalty in 2020 for data governance and risk management failures. Banks that can't demonstrate auditable, controlled AI systems face the same penalty risk — and AI governance failures will be harder to defend than data management ones.

Frequently Asked Questions

How does machine learning detect fraud faster than traditional rule-based systems in banking?

ML models analyze hundreds of behavioral signals simultaneously, scoring each transaction or event within seconds. Rule-based systems match against a finite list of pre-coded conditions; any novel pattern bypasses them entirely. ML learns from historical data, so it catches threats that no one has explicitly anticipated.

What types of threats can ML-based systems detect in real-time banking environments?

The range covers payment fraud, account takeover, synthetic identity fraud, insider data exfiltration, and phishing-based credential theft. In AI-enabled banks, ML operating at the inference layer also detects prompt injection, jailbreaks, and retrieval poisoning targeting AI agents: threat categories that transaction-layer fraud models were never designed to see.

How do banks manage false positives in ML-driven threat detection?

Modern ML systems use behavioral baselines, risk scoring, and continuous retraining to reduce false positives significantly compared to rule-based approaches. Explainable AI outputs allow analysts to quickly validate or dismiss flagged events, reducing the investigation time that alert fatigue creates under legacy tools.

What is the difference between supervised and unsupervised machine learning for banking security?

Supervised learning detects known threat patterns using labeled training data, making it effective for payment fraud with established historical precedent. Unsupervised learning identifies anomalies without labels, making it essential for catching novel attacks or insider threats that have no prior examples to match against.

What regulations govern the use of AI and ML for security in banking?

Key US frameworks include the FFIEC IT Handbook on AI/ML risks, OCC bulletins OCC 2011-12 and SR 11-7, and the NIST AI RMF. International operations also fall under the EU AI Act. Across all frameworks, banks must demonstrate model explainability, auditability, and documented risk controls.

How are AI agent attacks different from traditional banking cyber threats, and can ML detect them?

AI agent attacks, including prompt injection, jailbreaks, and retrieval poisoning, target the AI decision layer rather than the network or transaction endpoint, where traditional fraud models have no visibility. Detection requires ML-based runtime enforcement at the inference level, evaluating each agent action before it executes, not the transaction monitoring tools most fraud teams currently rely on.