Introduction

Financial institutions face a paradox at the center of their AI strategies: the same technology making fraud detection faster and compliance automation more reliable is being turned against them by increasingly sophisticated adversaries.

IBM's 2024 Cost of a Data Breach report puts the average financial-sector breach cost at $6.08 million—22% above the global average—with breaches taking 168 days to identify and another 51 days to contain. Those timelines expose a security model that wasn't built for the current threat environment.

Traditional security tools—firewalls, DLP systems, code scanners—were built for a different threat surface. They weren't designed to catch prompt injection in a loan processing workflow, poisoned retrieval in a compliance assistant, or unauthorized tool calls from an autonomous agent. As banks accelerate AI adoption, that gap is widening fast.

This article covers what that means practically: how AI strengthens banking defenses, what the new AI-native attack surface looks like, what regulators expect, and how to build a security strategy that keeps pace with both.

Key Takeaways

- AI-powered fraud detection, UEBA, and behavioral biometrics are now core banking defenses—and attackers are using the same techniques to get past them

- Prompt injection, jailbreaks, retrieval poisoning, and unsecured multi-agent handoffs are the fastest-growing AI-native threats, invisible to conventional security stacks

- NIST AI RMF, OWASP LLM Top 10, and the EU AI Act are converging into a compliance baseline requiring explainable, auditable AI decision trails

- Layered AI security combines ML-based detection, runtime enforcement, and governance controls—no single tool closes the gap alone

- Banks that embed security at deployment cut breach costs, reduce alert fatigue, and shrink regulatory exposure from day one

The High Cost of Cybercrime in Banking: Why AI Is Now Essential

The financial sector isn't just a frequent target — it's the costliest industry for breach recovery. The numbers reflect how much ground attackers have already taken:

- The average breach costs a financial firm $6.08M per incident

- A breach exposing 50 million or more records carries an average price tag of $375 million

- FIS and Oxford Economics estimate annual losses from cyberthreats, fraud, and operational inefficiencies at $98.5M per organization — a figure that includes operational drag beyond pure cyber losses

Legacy Infrastructure Is Making Things Worse

The OCC has flagged that prolonged reliance on legacy systems creates serious security risks: end-of-life software, unpatched vulnerabilities, fragmented data architectures, and reduced operational resilience. These aren't abstract concerns. Legacy infrastructure directly limits a bank's ability to deploy AI-driven fraud detection, automate compliance monitoring, or respond to threats in real time.

Technical debt creates a gap between where attackers operate and where defenses can reach. That gap translates directly into longer dwell times, slower containment, and higher breach costs — three outcomes regulators are increasingly unwilling to accept.

How Boards Started Paying Attention

The 2014 JPMorgan Chase breach — affecting an estimated 76 million households and 7 million small businesses — forced cybersecurity onto board agendas across the industry. JPMorgan responded by spending more than $250 million on cyber capabilities that year, doubling security personnel, and establishing three global security operations centers. Cybersecurity moved from back-office concern to board-level priority across the industry almost overnight.

A decade later, that priority has only intensified — and the attack surface has shifted. AI deployments now introduce threat vectors that firewalls, DLP tools, and code scanners weren't built to handle: prompt injection, retrieval poisoning, and autonomous agent actions that execute before any human reviews them.

How AI Defends Banks Against Cyber Threats

Fraud Detection and Anomaly Detection

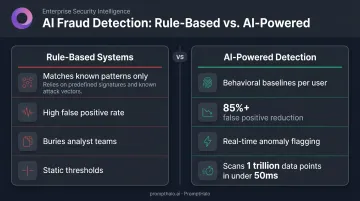

Rule-based fraud systems work by matching transactions against known patterns. The problem: sophisticated fraud doesn't follow known patterns, and high thresholds generate enough false positives to bury analyst teams.

ML-based systems take a different approach. They establish behavioral baselines for individual users and flag deviations in real time—catching anomalies that static rules miss entirely. Mastercard's Decision Intelligence Pro illustrates what this looks like at scale: the system improved fraud detection by 20% on average (up to 300% in some cases), reduced false positives by more than 85%, and scans one trillion data points in under 50 milliseconds.

For banks, that false-positive reduction matters as much as detection improvement. Every unnecessary alert consumes analyst time and creates alert fatigue that causes real threats to be missed.

Automated Threat Intelligence and Zero-Day Response

Manual threat analysis doesn't scale. Security teams can't process dark web forum activity, traffic logs, and external threat feeds simultaneously, prioritize them accurately, and act fast enough to stop emerging attacks.

AI automates that aggregation and pattern recognition. It surfaces risk signals that human analysts would miss and prioritizes response based on severity—not arrival order. This is particularly valuable for community and mid-size banks with lean security teams who face the same threat landscape as large institutions with a fraction of the analyst capacity.

The IBM data on breach lifecycle—168 days to identify, 51 days to contain—reflects what happens without automated detection. Institutions using AI and security automation saved an average of $1.9 million compared to those that didn't, according to the same IBM research.

User and Entity Behavior Analytics (UEBA) and Behavioral Biometrics

UEBA builds dynamic baselines from observable inputs:

- IP addresses and login locations

- Access timing and session patterns

- Device fingerprints

- Transaction sequences and amounts

When behavior deviates from that baseline—an employee accessing systems at unusual hours, a login from an unfamiliar location, a transaction sequence outside a customer's history—UEBA triggers an alert before damage occurs. That makes UEBA particularly effective against insider threats and account takeovers, where credentials are valid but behavior is suspicious.

Behavioral biometrics extend this into a passive authentication layer. The FFIEC recognizes the following signals as meaningful controls for high-risk transactions:

- Keystroke dynamics and typing cadence

- Finger swipe and tap behavior

- Mouse movement patterns

These signals are extremely difficult to replicate, even with stolen credentials. And because they're collected passively, they add no friction for the customer.

Anti-Phishing and Social Engineering Defense

According to APWG's Q4 2024 Phishing Activity Trends Report, financial institutions represented 11.9% of all phishing targets—nearly 118,000 attacks in a single quarter. AI-powered email security counters this by analyzing sender authentication signals (DKIM, DMARC, SPF), metadata patterns, and message content simultaneously, separating legitimate communications from spoofing attempts far more accurately than signature-based filters.

FinCEN's 2024 alert on deepfake media fraud (SAR keyword: FIN-2024-DEEPFAKEFRAUD) signals the harder problem: the same AI capabilities enabling better phishing defense are being weaponized for voice impersonation and synthetic identity attacks. Threat and defense are advancing together, which means detection systems need to keep pace with generative techniques, not just legacy signatures.

AI-Native Threats: The New Attack Surface Banks Can't Ignore

Traditional cyberattacks target infrastructure—networks, endpoints, applications. AI-native attacks target something different: the decision-making layer of AI systems themselves.

As banks deploy LLM-based assistants, agentic workflows, and RAG retrieval systems, attackers gain the ability to manipulate what those systems do. Not by breaking in, but by feeding them manipulated instructions. Firewalls, DLP tools, and code scanners weren't designed to see this attack surface at all.

Prompt Injection and Jailbreaks

OWASP ranks prompt injection as the top LLM security risk. In a banking context, the attack is straightforward: a malicious instruction embedded in a customer message, uploaded document, or external data source hijacks what the AI agent does next.

The consequences in financial services aren't theoretical. An injected instruction could authorize a fraudulent transaction, exfiltrate account data, bypass a compliance check, or override an approval threshold, all without triggering a single traditional security alert. Jailbreaks operate similarly, using crafted inputs to push a model outside its safety constraints.

Retrieval Poisoning in RAG Systems

Many banking AI applications use Retrieval-Augmented Generation: the model queries an external knowledge base before responding. That retrieval layer is an attack surface.

Retrieval poisoning corrupts the knowledge base the AI queries. A manipulated document in the retrieval store can cause an AI compliance assistant to surface incorrect regulatory guidance, generate a falsified transaction history, or produce a flawed credit decision— silently, with no visible system error. The model is working exactly as designed. The inputs are wrong.

Multi-Agent Handoff Risks

Banks are increasingly chaining AI agents together for complex workflows: loan processing, KYC automation, fraud triage. Each handoff between agents is a trust boundary.

If authority and scope aren't enforced at every decision point, an agent can inherit more permissions than it should have, carry a compromised instruction across the chain, or invoke tools outside its intended scope.

The risk compounds with each additional agent in the workflow. A single exploited handoff can propagate through an entire automated process before any human sees the output.

Closing the Gap with Runtime Enforcement

Conventional tools inspect code and monitor perimeters. They don't evaluate individual inference decisions, tool calls, or agent handoffs in real time.

Runtime AI security fills that gap. PromptHalo's enforcement engine sits inline on every inference, tool call, and agent-to-agent handoff, deciding to allow, restrict, challenge, deny, or monitor each action in under 100ms.

Detection combines threat library signatures with classifier-based risk scoring, achieving a catch rate above 95% at under 5% false positives, compared to roughly 35% catch rate and 15–20% false positives for rule-based approaches.

At agent handoff points specifically, the platform applies:

- Security passports that carry policy and authority information across multi-agent workflows

- Authority decay mechanisms that prevent privilege accumulation over time

- Per-action budget enforcement that stops agents from invoking tools beyond their intended scope

Together, these controls mean a single misconfigured handoff doesn't become a full-chain compromise.

AI Governance and Regulatory Compliance in Banking

The regulatory landscape for AI in banking has moved fast. Banks now operate under overlapping frameworks that collectively require explainability, auditability, fairness monitoring, and documented risk management for AI systems.

US Regulatory Framework

Key requirements currently in play:

- SR 11-7 / Model Risk Management: FDIC, Federal Reserve, and OCC issued revised interagency guidance in 2026, requiring robust governance, independent validation, ongoing monitoring, and outcomes analysis for models—including AI

- NCUA: Developing AI-specific guidelines and policies; GAO recommended NCUA update model risk management examination procedures for credit unions

- Treasury: Released a 2024 report on managing AI-specific cybersecurity risks, recommending focused risk management and industry collaboration

- House Financial Services: 2024 AI working group priorities included bias and discrimination, GLBA/FCRA data privacy, consumer protection, and applying existing laws to AI systems

Global Convergence

The EU AI Act entered into force in August 2024. For banking, the most significant provision classifies AI used to evaluate creditworthiness or establish credit scores as high-risk—triggering requirements for risk management systems, data governance, technical documentation, human oversight, and cybersecurity measures. Most high-risk obligations apply from August 2026.

NIST AI RMF's Govern-Map-Measure-Manage structure and OWASP LLM Top 10 have become de facto compliance baselines for any bank operating internationally or working with multinational fintech partners.

What This Means for Audit Logging

Regulators expect banks to maintain evidence of how AI systems make decisions—not just that they produce acceptable outputs. That means decision-level logs that capture what the AI did, why, under what authority, and in what context.

PromptHalo generates append-only, tamper-evident audit logs at the decision level: every action is recorded with its reason, the acting agent's identity, session and tenant context, and a timestamp. The format is designed to support compliance export and post-incident investigation without requiring a separate compliance layer.

Third-Party AI Risk

Banks are accountable for vendor-supplied AI tools under the same frameworks that govern internal systems. Contracts should include data ownership provisions, audit rights, and performance benchmarks. Vendor AI should be subject to the same runtime monitoring applied to internally developed models.

That requirement extends to vendor tools as well. PromptHalo's model-agnostic architecture—compatible with OpenAI, Anthropic, Azure OpenAI, and open-source models—applies the same monitoring and enforcement to third-party AI without requiring access to or modification of the underlying model.

Building a Layered AI Security Strategy for Banking

No single tool closes the AI security gap. The approach that works combines governance structure, technical enforcement, and external collaboration.

Start with Governance

Establish a cross-functional AI governance committee—compliance, IT, risk, and business units—before deployment decisions are made. Define acceptable use cases, set approval workflows, and treat AI systems as critical infrastructure within the existing cybersecurity strategy.

Done right, governance prevents banks from deploying AI systems that generate regulatory exposure faster than they generate business value.

Layer the Technical Defenses

A practical defense model builds in stages:

- AI-driven monitoring for routine, lower-risk tasks—establishing behavioral baselines and surfacing anomalies

- Runtime enforcement for high-risk agentic actions—inline decisions on every tool call and agent handoff

- Compliance controls at the architectural level—operating continuously without blocking innovation or degrading customer experience

- Continuous human oversight—catching model drift, bias, and adversarial manipulation that automated systems might miss

Platforms like PromptHalo integrate into this stack in under a day—no model retraining, no code rewrite—and enforce custom security rules per action at the point of decision, not after the fact.

Collaborate Beyond the Institution

Banks cannot detect emerging AI-native attack patterns in isolation. FS-ISAC released six AI-risk white papers in 2024 specifically to support structured threat intelligence sharing across financial services. The FSB has flagged AI in financial services as having financial-stability implications requiring cross-sector governance.

Those frameworks exist to be used. Sharing threat intelligence with peers, regulators, fintech partners, and payment service providers helps institutions identify new attack patterns before they spread. The community-level response to AI-native threats is still forming—early participation in those networks compounds over time.

Frequently Asked Questions

How is AI used in digital banking?

AI powers fraud detection and real-time anomaly monitoring, personalized customer service through chatbots and product recommendations, compliance automation, credit risk scoring, and increasingly agentic workflows that execute multi-step financial tasks autonomously—such as loan processing, KYC checks, and transaction routing.

Are banks safe with AI?

AI makes banks significantly more capable of detecting and responding to threats. However, it also introduces new vulnerabilities, particularly in agentic deployments where autonomous agents can be manipulated through prompt injection, retrieval poisoning, or unsecured handoffs. Those risks require purpose-built runtime security and continuous monitoring that operate alongside the AI deployment itself.

What are the 4 types of AI risk?

The four commonly cited categories are: model/algorithmic risk (bias, drift, adversarial manipulation), operational risk (system failures, data quality issues), compliance/regulatory risk (explainability and auditability requirements), and strategic risk (misaligned AI objectives or third-party dependency).

Which AI is best for digital banking services?

Effective banking AI stacks typically combine ML-based fraud detection, NLP for customer interactions, and behavioral analytics for authentication. For agentic deployments, that stack also needs runtime security enforcement to protect every agent decision in regulated workflows from manipulation.

What are the biggest AI-specific security risks banks face today?

Prompt injection, jailbreaks, retrieval poisoning in RAG systems, and unsecured multi-agent handoffs are the fastest-growing AI-native threats. These vectors bypass traditional perimeter defenses entirely and require inline, decision-level enforcement evaluated at the moment of each agent action.