The numbers frame the stakes: global card fraud losses reached $33.83 billion in 2023, with projections pointing toward $403.88 billion in cumulative losses over the next decade. Meanwhile, RTP network volume hit 343 million transactions in 2024, up 38% year-over-year. FedNow volume in 2025 grew 458.9% from the prior year.

At that scale and speed, rule-based fraud systems aren't just inefficient — they're structurally inadequate.

This article covers how AI-powered real-time fraud detection works in 2026, what new threats are emerging (including fraudsters weaponizing AI against your detection systems), and what security and risk teams need to do to stay ahead.

Key Takeaways

- Real-time payment rails eliminate the buffer for human review — fraud detection must operate in milliseconds

- AI replaces brittle IF-THEN rules with dynamic, probabilistic risk scoring across hundreds of signals simultaneously

- Deepfake fraud, synthetic identity schemes, and AI-optimized credential stuffing are the dominant 2026 threat vectors

- Agentic AI fraud systems create a new attack surface: prompt injection and RAG poisoning can manipulate LLM-based decisioning

- Governance, explainability, and tamper-evident audit logs are now regulatory requirements, not optional add-ons

Why the 2026 Payments Landscape Demands Real-Time AI Fraud Detection

The Zero-Latency Problem

Instant payment networks have eliminated something fraud teams relied on for decades: time. Batch processing gave investigators hours to review suspicious transactions before funds cleared. Real-time rails give them milliseconds.

The Federal Reserve's 2026 Risk Officer Survey — drawn from 403 U.S. financial institution risk experts — shows instant payment fraud attempts are climbing: 15% of institutions reported fraud attempts on real-time rails, up 3 percentage points from the prior year. In the UK, Faster Payments carried 98% of all fraudulent authorized push payment transactions by volume, according to UK Finance's 2024 Annual Fraud Report.

The infrastructure has scaled faster than the defenses protecting it.

Where Rule-Based Systems Break Down

Traditional rule-based fraud systems apply fixed logic: flag any transaction over $10,000 from a new device, block international transfers from accounts with no prior history. The problem is that fraudsters know the rules too.

Static thresholds create predictable evasion paths. More damaging, they generate excessive false positives. Two findings illustrate the scale of the problem:

- One in three institutions reported "high" or "very high" false positive rates from their fraud detection systems, according to FICO's 2026 global financial institutions survey

- 44% of U.S. financial services firms still relied mostly or entirely on manual review processes in 2025, per LexisNexis Risk Solutions — an unsustainable model at real-time payment volumes

Rule-based systems also require manual updates whenever fraud patterns shift. Against adversaries who iterate in hours, that lag is decisive.

The Professionalization of Fraud

Modern fraud operations are industrialized. Fraud-as-a-service kits, infostealer malware marketplaces, and AI-optimized credential stuffing tools have lowered the barrier to entry while expanding attack scale. Fraudsters now test stolen credentials against thousands of platforms simultaneously, pivot quickly when detection patterns emerge, and increasingly use AI to probe fraud systems for exploitable thresholds.

The attack surface isn't static — and neither are the attackers running it. Rule-based controls that update on a quarterly patch cycle are fundamentally mismatched against adversaries who iterate daily.

How AI-Powered Real-Time Fraud Detection Works

The fundamental shift in AI-driven fraud detection is from binary decisions to probabilistic risk scoring. Rather than asking "does this transaction break a rule?", AI models ask "given everything we know about this customer, this device, this merchant, and this moment: how anomalous is this?"

That distinction matters enormously in practice. A $3,000 wire transfer might be routine for one customer and a four-alarm signal for another.

Behavioral Profiling and Anomaly Detection

AI fraud systems build individual behavioral baselines for each customer — learning typical transaction amounts, device usage patterns, geolocation history, merchant categories, and payment velocity. When a transaction deviates from that learned norm, it's scored in context rather than against a universal threshold.

This matters because context changes everything. An international wire from an account that has only ever made domestic ACH payments is genuinely anomalous. A $5,000 purchase from a new merchant is normal for a frequent traveler.

Detecting those contextual deviations gets harder at the edges of known fraud patterns. Unsupervised ML techniques (isolation forests, autoencoders, clustering algorithms) extend this capability by identifying outliers that fall outside learned norms without requiring labeled fraud examples — making them particularly effective against novel attack vectors that supervised models haven't encountered before.

Graph-Based Network Analysis

Individual transaction-level analysis misses coordinated fraud. Mule account networks, synthetic identity rings, and first-party fraud schemes often look legitimate at the account level while revealing clear patterns when relationship data is mapped.

Graph neural networks connect accounts, devices, merchants, and IP addresses into a relational structure where hidden patterns become visible. None of these signals are detectable in isolation, but they become obvious once relationship data is mapped:

- A device registered across 40 separate accounts

- A merchant receiving transfers from accounts opened within the same 48-hour window

- An IP address surfacing across seemingly unrelated fraud attempts

Each of these is invisible in a single-account view. In a graph, they're glaring.

Real-Time Risk Scoring and Dynamic Response

Speed is non-negotiable. AI fraud systems must complete risk evaluation within the payment authorization window — typically sub-100ms — without degrading the payment experience.

The standard tiered response model works as follows:

- Low risk: Transaction passes through without friction

- Medium risk: Step-up authentication triggered (SMS OTP, push notification)

- High risk: Transaction blocked or routed to analyst queue

An all-or-nothing block/approve approach generates the false positives that erode customer trust and suppress approval rates. The graduated model threads that needle — applying friction proportional to actual risk, not assumed risk.

The Evolving 2026 Fraud Threat Landscape

Deepfakes and AI-Enhanced Social Engineering

Generative AI has given fraudsters a capability that didn't exist at scale three years ago: convincing synthetic identities. Audio clones, video deepfakes, and fabricated identity documents can now be produced quickly enough to target financial institutions at volume — bypassing KYC verification and biometric checks that were designed for a pre-generative-AI threat environment.

The scale is significant. Deloitte projects that generative AI could drive U.S. fraud losses to $40 billion by 2027, up from $12.3 billion in 2023 — a 32% compound annual growth rate. FinCEN issued a formal alert in 2024 documenting increased suspicious activity reports involving deepfakes used to circumvent identity verification at financial institutions.

Synthetic Identity Fraud

Synthetic identities combine real data elements (a valid Social Security number, a real address) with fabricated details to create identities that pass credit checks, open accounts, and build behavioral histories. They're designed to look legitimate for months or years before a "bust-out" event.

TransUnion estimates U.S. lenders faced more than $3.3 billion in synthetic identity fraud exposure in 2024. Detecting these schemes requires cross-system intelligence — connecting KYC data, card issuance records, HR systems, and transaction behavior — not just transactional anomaly detection at the payment rail level.

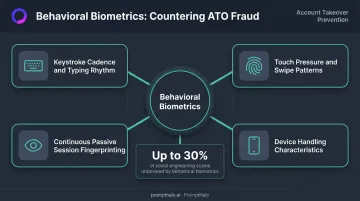

Account Takeover Amplified by AI

ATO fraud losses were projected to reach $17 billion in 2025, with fintech and finance ATO attacks increasing 122% year-over-year, according to Sift's Q3 2025 Digital Trust Index. The primary driver: AI-optimized credential stuffing tools that test stolen credentials at massive scale, then pivot attack patterns the moment they detect increased friction.

The most effective countermeasure has shifted from static authentication to behavioral biometrics: passive signals that are difficult to steal and nearly impossible to replicate. These include:

- Keystroke cadence and typing rhythm

- Touch pressure and swipe patterns

- Device handling characteristics

- Continuous passive fingerprinting across a session

BioCatch reported that behavioral biometrics analysis uncovered up to 30% of social engineering scams that evaded other detection methods in a 2025 Australian banking study.

The Emerging Blind Spot: When Your Fraud Detection AI Becomes the Target

Here's the threat most risk teams aren't fully accounting for yet: as financial institutions deploy LLM-based agents to automate fraud decisioning, AML alert triage, and compliance workflows, those agents create a new attack surface. The instructions and data flowing into the model can be manipulated — without ever touching the underlying model or infrastructure.

What Prompt Injection Looks Like in Payments

Prompt injection in a payment context doesn't require a sophisticated technical exploit. A bad actor can embed adversarial instructions within a transaction description, a customer-submitted document, or retrieved data in a RAG pipeline. When an LLM-based fraud review agent processes that content, the injected instruction can cause it to suppress a flag, approve a transaction, or leak account context, all while appearing as normal model behavior to external observers.

NIST's adversarial machine learning guidance (AI 100-2e2025) specifically identifies indirect prompt injection — where malicious instructions embedded in external resources hijack generative AI systems — as a primary threat category. OWASP LLM Top 10 lists prompt injection as the leading runtime AI risk, alongside retrieval poisoning and insecure output handling.

Why Traditional Security Controls Miss This

Firewalls, DLP tools, and code scanners inspect infrastructure. They examine network traffic, file transfers, and application code. They cannot inspect what happens inside an AI inference call, a RAG retrieval, or an agent-to-agent handoff. The attack surface is the model's behavior, not the network perimeter.

This is a new category of vulnerability, and most security stacks were not built to address it.

Runtime AI Security as the Solution

Addressing this requires purpose-built tooling that operates where the risk actually lives: inside the inference. PromptHalo sits inline on every inference, tool call, and agent handoff, making per-action decisions in under 100ms before execution. The detection layer combines embedding-based scoring against a shared threat library with classifier-based risk scoring, achieving a catch rate above 95% at under 5% false positives.

The platform's design is a closed-loop defense. The Red Teaming solution continuously probes agents, RAG layers, and tool chains to surface exploitable paths before they ship. Attack patterns discovered during that probing are encoded directly into the shared Threat Library, making them immediately enforceable by the Runtime Security layer without waiting for a new release cycle.

Key enforcement mechanisms include:

- Security passports: Signed credentials that travel with each agent request, encoding policy, budget, and authority parameters

- Authority decay: Agent permissions diminish over time and usage, forcing re-authorization when envelopes are exceeded

- Per-action scope enforcement: Every tool call and API invocation is evaluated against defined boundaries before execution

- Tiered response: Each action receives one of five decisions (allow, restrict, challenge, deny, or monitor), backed by a tamper-evident audit log

The platform deploys in under a day with no model retraining and no code rewrite, and works across any AI application from any vendor.

Building Governance, Auditability, and Compliance Into AI Fraud Systems

Explainability Is Now a Legal Requirement

Regulators have been clear on this. The CFPB's Circular 2022-03 established that creditors using complex algorithms must provide specific, accurate adverse action reasons — "black box" is not a defense. Circular 2023-03 reinforced that AI models cannot substitute closest-matching checklist reasons when those reasons don't reflect the actual factors used.

Three frameworks now define the baseline for fraud AI governance:

- CFPB Circulars 2022-03 and 2023-03: Require specific, accurate adverse action explanations — no substituting checklist reasons that don't reflect actual model factors

- EU AI Act (full high-risk obligations from August 2026): Classifies creditworthiness AI as high-risk; fraud detection has a carve-out, but documentation, governance, and oversight requirements still apply

- NIST AI RMF 1.0: Organizes AI risk management around Govern, Map, Measure, and Manage, with explicit emphasis on accountability, transparency, and lifecycle documentation

Human-in-the-Loop Remains Non-Negotiable

Effective AI fraud governance doesn't mean full automation. High-risk or novel fraud decisions benefit from human review, particularly when:

- Model confidence falls below defined thresholds

- The transaction pattern is genuinely novel with no training analog

- The fraud typology involves complex multi-party schemes

The practical architecture includes confidence thresholds below which cases route to analyst queues, escalation protocols for edge cases, and feedback loops where analyst decisions retrain models over time. Automation handles volume; humans handle complexity.

Audit Trail Quality as a Competitive Differentiator

Replayable, decision-level logs are no longer just a compliance checkbox. When regulators or customers ask "why did your system make that decision?" the quality of your audit trail determines whether that conversation is routine or damaging.

PromptHalo's audit logs capture every decision along with its reason, the acting agent identity, session and tenant context, and a timestamp. The logs are append-only and tamper-evident, creating a replayable evidence trail that supports debugging, compliance export, and post-incident investigation. For security teams working against OWASP LLM Top 10, NIST AI RMF, and the EU AI Act, that documentation depth is what makes an audit manageable — not a scramble.

Frequently Asked Questions

Can AI be used to detect fraud in real time?

Yes. AI-powered systems analyze transactions during the authorization window (typically under 100ms), scoring risk across hundreds of behavioral and contextual signals before a payment clears. This makes real-time fraud prevention both technically feasible and now standard for fintech and banking environments.

Which AI model is commonly used for fraud detection?

No single model dominates. Effective systems layer supervised ML (gradient boosting, random forests) for known fraud patterns, unsupervised ML (autoencoders, isolation forests) for novel attacks, and graph neural networks for fraud ring detection. Generative AI is increasingly used for alert summarization and analyst support.

What are the 3 C's of fraud?

The 3 C's are Concealment, Conversion, and Conspiracy — describing how fraudsters hide illicit activity, convert stolen assets into usable form, and operate through coordinated networks. AI-powered graph analysis and behavioral monitoring are particularly effective at surfacing all three dimensions simultaneously.

What is the difference between rule-based and AI-powered fraud detection?

Rule-based systems apply fixed IF-THEN logic. AI systems evaluate transactions against dynamic behavioral baselines, adapt to new tactics without manual updates, and make probabilistic decisions rather than binary ones — significantly reducing false positives in the process.

How do false positives affect payment businesses, and how does AI reduce them?

False declines frustrate customers, increase churn, and suppress approval rates. AI reduces them by understanding each customer's normal behavioral variance, distinguishing unusual-but-legitimate transactions from genuine fraud through context rather than fixed thresholds.