Introduction

Agentic AI is rewriting how commerce works. Shopping agents browse catalogs, compare prices, and execute purchases without a human pressing "confirm." According to Juniper Research, agentic commerce spend is forecast to reach $1.5 trillion globally by 2030. That projection lands inside most enterprise planning horizons — which means compliance governance can't wait for 2030.

The problem is structural. Security teams and compliance officers in fintech and payments are now responsible for governing AI that executes transactions, accesses financial data, and calls third-party APIs, without human confirmation at each step. Their existing playbooks weren't built for this.

Traditional DLP tools, firewalls, and rule-based controls catch what they were designed to see. They weren't designed to see an autonomous sub-agent exceeding its spending limit during a multi-step handoff, or payment tokens leaking through a reasoning trace.

This guide addresses that gap directly:

- Why legacy compliance frameworks break down for agentic AI

- The specific enforcement challenges emerging in 2026

- The regulatory landscape — EU AI Act, NIST AI RMF, and OWASP LLM Top 10

- Practical steps for building a compliant agentic stack

Key Takeaways

- Traditional DLP, firewalls, and rule-based controls miss the agentic AI attack surface, especially during multi-agent handoffs and autonomous tool calls.

- Regulations like GDPR, CCPA, KYC/AML, and PCI-DSS assume human decision-makers and don't map cleanly to autonomous agent transactions.

- "Know Your Agent" (KYA) is the 2026 equivalent of KYC: commerce systems must cryptographically verify agent identity before executing any transaction.

- Decision-level audit trails are a regulatory expectation under the EU AI Act and NIST AI RMF, not just a security best practice.

- Runtime enforcement, not model training, is the only reliable way to maintain compliance as agentic commerce scales.

Why Existing Compliance Frameworks Fail for Autonomous AI Agents

Every major commerce and financial regulation—GDPR, CCPA, PCI-DSS, KYC/AML, the Bank Secrecy Act—attaches obligations to controllers, financial institutions, businesses, and systems. None of them contemplate an autonomous agent as the accountable actor.

The agent acts on inferred intent and executes in milliseconds. That fundamental mismatch creates at least four distinct failure modes.

The Consent Chain Problem

When a user grants permission to a primary agent, that agent may delegate authority to a sub-agent or third-party agent service. The EDPB requires consent to be specific, informed, and as easy to withdraw as to give. In practice, the original consent scope rarely travels intact through the delegation chain.

A user might consent to "find the cheapest flight." By the time a sub-agent has queried payment, loyalty, identity, and merchant systems, it has accessed data under purposes the user never authorized. That's a purpose limitation violation under GDPR—and it happens without any visible breach.

The Liability Attribution Gap

When an AI agent makes an unauthorized purchase or leaks payment data, the question of who bears liability—merchant, platform, agent provider, or consumer—remains largely unresolved. Legal analysis from 2025 argues that AI agents can generate outcomes developers or deployers cannot fully anticipate, calling for targeted legal adaptation rather than wholesale regulatory replacement.

Commerce platforms should document principal, agent, merchant, platform, and regulated-institution duties contractually rather than waiting for courts to resolve this.

Speed vs. Review Mismatch

Compliance review cycles were designed for human-paced decisions. The FCA has noted that AI agents may initiate, route, and optimize transactions on consumers' behalf at speeds that create new AML and consumer-protection challenges. Real-time human review is impossible at agent velocity. This forces a shift toward automated, policy-driven enforcement at the point of action—not post-hoc review.

Data Sovereignty Across Borders

That same velocity extends the blast radius across borders. Agentic systems operating across geographies can pull customer data from multiple jurisdictions in a single session. Overlapping regulatory obligations—GDPR for EU residents, CCPA for California, and others—become nearly impossible to satisfy without programmatic controls on data access at the tool call level. Without enforcement at that granular level, a single session can silently generate liability across three or four frameworks before a human reviewer sees the first log entry.

The Major Compliance Challenges in Agentic Commerce for 2026

Data Privacy and Consent Management

GDPR and CCPA require explicit, specific consent for data use. Agentic AI routinely ingests preference data, purchase history, and behavioral signals from multiple sources to make decisions. As agents increasingly aggregate data across merchants for replenishment and recommendations, they can violate the purpose limitation principle without any visible breach event.

The scale here matters. Visa's 2025 research found one in three consumers expect to use AI shopping agents regularly—but 85% demand explicit data control. Adoption is possible only if the stack can prove data use and action authority at each step.

Granular, revocable consent is the harder problem. Regulations require users to withdraw consent and have data deleted—but by the time a user requests deletion, an agentic system may have already distributed that data across multiple tool calls, RAG retrievals, and sub-agents. Making deletion tractable requires:

- Encoding consent as a machine-enforced mandate with purpose, merchant category, data categories, payment limit, expiry, and revocation endpoint

- Tracking which specific data sources and retrievals each agent session accessed

- Enforcing that sub-agent delegation is only permitted when the original consent scope explicitly allows it

Financial Compliance: KYC, AML, and Autonomous Payments

No regulator has yet issued explicit guidance on how KYC/AML applies when a consumer AI agent executes a cross-border or high-value payment autonomously. The FCA comes closest, stating that AI agents may initiate, route, and optimize transactions in ways that create new AML and consumer-protection challenges—without yet imposing AI-specific regulations.

PCI-DSS is directly applicable wherever an agentic system stores, processes, or transmits cardholder data. In practice, that means payment credentials, PANs, and reusable tokens must never appear in prompts, tool-call traces, reasoning logs, or vector stores. Any tool chain that touches payment data is subject to PCI-DSS controls across:

- Encryption and access restriction

- Authentication at each processing step

- Logging and audit trail completeness

The fraud risk is already real. Feedzai's 2025 survey of 562 global fraud and financial-crime professionals found 92% of financial institutions report that fraudsters are already using generative AI. A separate Alloy report found 60% of financial institutions and fintechs saw fraud increase in 2024. Prompt injection attacks targeting commerce agents—designed to redirect payments or exfiltrate tokens—are an active vector, not a theoretical one.

Multi-Agent Accountability and Scope Enforcement

The authority decay problem is where compliance failures concentrate in multi-agent systems. A user authorizes Agent A with a defined budget and scope. Agent A delegates a subtask to Agent B. Agent B has no direct relationship with the original user—it only knows what Agent A told it.

Without explicit scope enforcement at each handoff, agents operate beyond their authorized boundaries. OWASP classifies this pattern as Excessive Agency: a system with too much functionality, too many permissions, or too much autonomy relative to what was authorized. The regulatory exposure is concrete: unauthorized autonomous action on a user's behalf can breach consumer-protection obligations regardless of whether a security incident occurs. Controls required at each handoff include:

- Per-action budget limits that decay as the agent operates

- Scope restrictions that prevent sub-agents from exceeding the original user mandate

- Authority verification at every agent-to-agent interaction, not just at the initial entry point

PromptHalo addresses this through agent security passports—signed credentials that travel with each request and carry policy, budget, and authority decay parameters. Authority is enforced externally at each handoff: an agent cannot grant itself more access than it was given, and budgets expire across time, steps, and risk thresholds.

Navigating the 2026 Regulatory Landscape

EU AI Act

The EU AI Act classifies AI systems used for creditworthiness assessment and credit scoring of natural persons as high-risk under Annex III. Shopping agents that influence BNPL eligibility, lending terms, or insurance pricing may trigger this classification. High-risk systems require risk management, technical documentation, record-keeping, transparency measures, human oversight, and post-market monitoring.

Article 2 of the EU AI Act applies to providers outside the EU where outputs are used in the Union. Non-EU agentic commerce providers serving EU consumers cannot avoid classification by hosting infrastructure outside Europe.

NIST AI RMF

For US enterprises operating without federal AI law, the NIST AI Risk Management Framework offers a structured governance foundation. Its four functions (Govern, Map, Measure, Manage) give compliance teams a clear method for identifying and mitigating AI risks in agentic deployments.

NIST also launched an AI Agent Standards Initiative in 2026 targeting agents capable of autonomous actions. The standards are still emerging — design agent identity, authority, logging, and oversight now rather than waiting for final guidance.

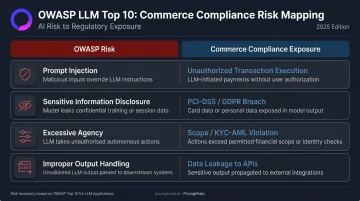

OWASP LLM Top 10 as a Compliance Bridge

OWASP's 2025 LLM Top 10 maps directly to compliance exposure in regulated commerce. Prompt injection, sensitive information disclosure, improper output handling, and excessive agency aren't just technical attack vectors—each one represents a potential regulatory failure:

| OWASP Risk | Commerce Compliance Exposure |

|---|---|

| Prompt Injection | Unauthorized transaction execution |

| Sensitive Information Disclosure | PCI-DSS violation, GDPR data breach |

| Excessive Agency | Scope violation, KYC/AML breach |

| Improper Output Handling | Data leakage to downstream APIs |

Mapping controls to the OWASP LLM Top 10 gives security teams an internationally recognized baseline — and gives regulators something concrete to evaluate when assessing your AI governance posture.

The US Regulatory Patchwork

Federal AI law doesn't exist yet. State-level privacy laws (CCPA, Virginia CDPA, Colorado SB24-205), FTC enforcement under Operation AI Comply targeting deceptive AI practices, and emerging state AI bills create a fragmented landscape. The practical approach: use the strictest applicable standard as your baseline and document your reasoning in your AI governance policies. This positions the enterprise to demonstrate compliance intent regardless of which framework a regulator applies.

The "Know Your Agent" Problem: Authentication and Fraud Compliance

KYC requires financial institutions to verify the identity of human customers before transacting. The 2026 equivalent for agentic commerce is Know Your Agent—verifying that an AI agent making a transaction is who it claims to be, has not been compromised, and is operating within its authorized scope.

Cloudflare's Verified Bots implementation provides the clearest technical specification currently available: cryptographic verification using Signature, Signature-Input, and Signature-Agent headers, where Signature-Agent points to a public key directory and the signature is verified with public-key cryptography.

Three major frameworks converge on the same underlying model:

- Cloudflare Verified Bots: Cryptographic header-based identity verification

- Visa's Trusted Agent Protocol: Signed mandates before a transaction executes

- FIDO's AP2 Framework: Verifiable intent attached to each agent action

Without cryptographic identity, merchants must infer legitimacy from behavioral patterns. That creates two failure modes:

- False positives: Legitimate agents exhibit unusual patterns—rapid sequential orders, cross-category purchases, unusual velocity—that look like compromised accounts to rules-based fraud systems. Valid transactions get blocked.

- False negatives: Adversarial bots mimic legitimate agent behavior patterns, bypassing fraud detection.

Fraud detection models need recalibration to distinguish authorized agent commerce from adversarial activity. Behavioral heuristics alone aren't sufficient, particularly given that 92% of financial institutions report fraudsters already using generative AI.

That detection gap makes the liability question urgent. When an agent transaction goes wrong, who bears responsibility: the merchant, consumer, agent platform, or AI provider? No clear legal standard exists yet. In this period of ambiguity, enterprises' best defense is audit trails that capture agent identity, authorization context, and decision signals at the moment of each transaction.

Building a Compliance-Ready Agentic Commerce Stack

Why Model-Level Guardrails Aren't Enough

Fine-tuned guardrails and RLHF-based safety training can be bypassed through prompt injection, jailbreaks, and novel attack paths. Gartner predicts over 40% of agentic AI projects will be canceled by end-2027 partly due to inadequate risk controls. Model-level safety measures are necessary but not sufficient—compliance for financial transactions and sensitive data handling requires enforcement that sits outside the model entirely.

A runtime enforcement layer evaluates every agent action inline before it executes, independent of the model. This is the only architecture that can handle the speed, scale, and adversarial creativity of production agentic commerce.

Minimum Viable Compliance Controls

| Control Layer | What It Does | Why It's Required |

|---|---|---|

| Agent identity verification | Cryptographic confirmation of agent identity and scope | KYA / fraud prevention |

| User mandate binding | Purpose, merchant category, payment limit, expiry, delegation permission | GDPR/CCPA consent |

| Payment boundary enforcement | PANs and tokens never enter prompts, logs, or tool traces | PCI-DSS |

| Runtime policy engine | Blocks out-of-scope API calls and data access inline | OWASP Excessive Agency |

| Decision-level audit logs | Captures reasoning context, tool calls, data accessed, enforcement decision | EU AI Act Art. 12, NIST RMF |

| Human escalation triggers | High-value, cross-border, or anomalous transactions require human approval | EU AI Act Art. 14 |

Each of these controls must operate at runtime, not as a post-hoc review layer. PromptHalo applies them on every inference, tool call, and agent-to-agent handoff in under 100ms, without touching the underlying model. Agent security passports travel with each request, carrying policy, budget, and authority decay parameters. When a budget envelope is exceeded or a scope boundary is reached, re-authorization is required before the agent can proceed.

Structuring Audit Trails for Regulatory Reporting

Transaction-level logs are not sufficient for agentic commerce compliance. Regulators and auditors need to reconstruct not just what happened, but why, with what authority, and using what data.

Compliant audit logs for agentic commerce must capture:

- Reasoning context: What the agent was attempting to do at the moment of decision

- Tool calls made: Every API call and external interaction, including sub-agent handoffs

- Data retrieved: Which sources and retrievals were accessed during the session

- Enforcement decision: What the runtime layer allowed, blocked, or escalated—and why

- Agent identity and passport: Which agent acted, under what authorization scope

- Timestamp and session context: Immutable record linking decisions to specific sessions

Logs should be append-only and tamper-evident. Once written, an event cannot be modified, creating a replayable evidence trail for debugging, compliance export, and post-incident investigation.

For enterprises operating under the EU AI Act, the operational priority is mapping these log fields to framework requirements before an audit begins. Teams that do this work upfront spend audit cycles producing evidence rather than reconstructing how their systems made decisions.

Frequently Asked Questions

What will be predicted in 2026 for agentic AI?

Agentic AI is moving from pilot to production scale in commerce and B2B workflows. Protocols are maturing rapidly—multi-item carts, subscription support, agent-to-agent transactions—alongside the emergence of KYA authentication standards and formal compliance frameworks as enterprise adoption accelerates.

What is the future of agentic commerce?

The trajectory runs from today's discovery-and-checkout agents toward full-lifecycle management: post-purchase, returns, proactive replenishment, and B2B procurement. The enterprises that win will have clean data infrastructure, compliant agentic stacks, and audit-ready systems—not necessarily the largest brand names.

What regulations currently apply to agentic AI commerce transactions?

Several frameworks apply, depending on jurisdiction and transaction type:

- EU AI Act — high-risk system requirements for credit and financial AI

- GDPR / CCPA — data privacy and consent obligations

- PCI-DSS — payment data handling standards

- KYC/AML — financial agent identity and anti-money-laundering rules

NIST AI RMF provides a voluntary US governance layer on top of these.

How do you maintain compliance when AI agents make autonomous purchasing decisions?

Runtime enforcement, not model-level guardrails, is the reliable mechanism. Granular scope and budget controls at each agent action, combined with decision-level audit logs capturing what the agent did and what authority it had, enable regulatory reporting without halting autonomous operation.

What is a "Know Your Agent" protocol and why does it matter for compliance?

KYA protocols are authentication standards (such as cryptographic header verification) that let commerce systems confirm an agent's identity, authorization scope, and integrity before a transaction executes. Think of them as KYC for AI agents: essential for fraud prevention and liability protection in agent-mediated commerce.

How should enterprises create audit trails for AI agent commerce actions?

Logs must capture reasoning context, tool calls, and data accessed at the decision level—not just transaction outcomes. They also need to be tamper-evident, replayable, and pre-mapped to OWASP LLM Top 10, NIST AI RMF, and the EU AI Act for efficient regulatory reporting.