It is. And if your compliance program wasn't built with that answer in mind, you have a gap.

According to the Bank of England and FCA's 2024 survey, 75% of UK financial services firms were already using AI—up from 58% in 2022. Meanwhile, IBM's 2025 research found that 63% of organizations lack AI governance policies, and 13% had already experienced attacks targeting AI models. The compliance infrastructure protecting payment environments was not designed for this.

PCI DSS 4.0.1 doesn't mention AI by name. But its control objectives apply in full—and AI introduces attack vectors that firewalls, DLP tools, and legacy code scanners simply cannot catch. This guide covers exactly where AI enters PCI scope, what new risks it creates, how the requirements map to AI system design, and what agentic AI means for compliance programs going forward.

Key Takeaways

- Any AI system that stores, processes, transmits, or influences cardholder data security falls within PCI DSS scope

- AI-native risks (prompt injection, retrieval poisoning, data leakage, model drift) fall outside what existing compliance tools were built to detect

- Requirements 3, 4, 7, 8, 10, and 12 have direct implications for AI system architecture, credentialing, and logging

- The PCI SSC's September 2025 AI Principles establish a clear baseline: AI complexity does not exempt any requirement

- Agentic AI—autonomous, multi-step, API-calling—is the next major compliance frontier

Why AI Systems Now Fall Under PCI DSS Scope

PCI DSS v4.0.1 applies to entities that "store, process, or transmit cardholder data and/or sensitive authentication data or could impact the security of the cardholder data environment (CDE)." That last phrase is the critical one.

An AI system doesn't need to store card numbers to be in scope. If it can query, influence, or interact with systems that do, it meets the threshold.

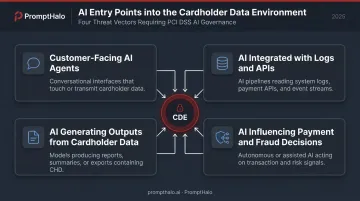

Four Ways AI Enters the Cardholder Data Environment

Most AI deployments touch the CDE through one of these entry points:

- Customer-facing AI agents handling billing queries, dispute resolution, or account inquiries—directly processing payment-related inputs

- AI systems integrated with logs, databases, or APIs containing transaction or account data

- AI generating outputs derived from cardholder data—summaries, reports, or recommendations built from sensitive records

- AI influencing decisions in payment or fraud flows—fraud scoring systems, approval models, or refund automation

Each creates scope because each can affect the confidentiality, integrity, or availability of cardholder data.

The "connected system" problem extends this further. An LLM-powered internal tool that can read transaction logs or trigger payment reversals is in scope—even if its system prompt never mentions card numbers. Capability determines scope, not content.

The Shift from Narrow Tools to Agentic AI

Early AI in payments (fraud scoring models, rules-based chatbots) was relatively contained. A fraud model receives a transaction and returns a score. Its scope footprint is limited and predictable.

Agentic AI operates differently. These systems autonomously call APIs, orchestrate multi-step workflows, retrieve from knowledge bases, and hand tasks off to other agents, often without a human approving each step. The CDE boundary — designed around discrete, human-operated system components — becomes genuinely difficult to enforce at that level of autonomy.

Gartner forecasts that 40% of enterprise applications will include task-specific AI agents by end of 2026, up from less than 5% in 2025. That adoption curve means compliance programs that haven't addressed agentic AI are already behind.

The PCI SSC's September 2025 AI Principles publication makes the position clear: operational complexity is not a compliance exemption. Organizations deploying agentic AI inherit the full scope of applicable PCI DSS requirements — and the enforcement burden of demonstrating control over systems that act autonomously.

AI-Native Risks That Threaten PCI DSS Compliance

Traditional compliance controls—firewalls, antivirus, legacy DLP—were built for a threat model centered on humans, networks, and files. AI introduces attack vectors that don't fit those categories and aren't caught by those tools.

Prompt Injection and Jailbreaks

OWASP ranks prompt injection as LLM01:2025—the top risk in its LLM Top 10. The attack works by crafting inputs that override an AI system's instructions, causing it to reveal sensitive data, perform privileged actions, or bypass security controls.

In a PCI-regulated environment, the stakes are direct: a manipulated AI agent could expose PANs, return account credentials, or initiate unauthorized transactions. This isn't theoretical—CVE-2025-32711, published June 2025, documents an AI command injection vulnerability in M365 Copilot allowing an attacker to disclose information over a network.

Jailbreaks are a related technique: rather than injecting instructions, attackers remove behavioral guardrails entirely. Both require detection at the inference layer, before the manipulated output executes — something rule-based filters alone can't reliably deliver.

Data Leakage and Model Memorization

Two distinct leakage vectors apply to AI systems in payment environments:

- Prompt-level leakage: Cardholder data included in prompts can surface in outputs, logs, or third-party inference API calls. Prompt histories stored without encryption and debug logs transmitted to AI vendors are both common, often undetected scope violations

- Model memorization: Per NIST AI 600-1, AI models may retain fragments of training or interaction data and surface it in future outputs—including sensitive data that was never intended to persist

OWASP's LLM02:2025 specifically identifies financial details as a category at risk of sensitive information disclosure through model outputs. Neither of these leakage paths produces network traffic patterns that legacy DLP tools are designed to catch.

RAG Retrieval Poisoning and Supply Chain Risk

Retrieval-augmented generation (RAG) systems pull from knowledge bases, document stores, or external data sources to inform AI responses. OWASP LLM08:2025 flags vector and embedding weaknesses as an exploitable attack surface: attackers who inject malicious content into those document stores can cause AI systems to return compromised outputs or take unauthorized actions. In payment environments where agents retrieve policy documents, pricing data, or customer records, this attack path is real.

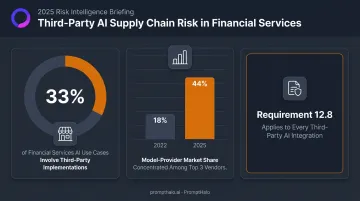

The supply chain exposure compounds the problem. Key numbers from recent financial services AI adoption data:

- 33% of financial services AI use cases involve third-party implementations

- 44% of model-provider share is concentrated among the top three providers — up from 18% in 2022

- Every third-party integration is a potential compliance surface requiring assessment under Requirement 12.8

Mapping PCI DSS v4.0.1 Requirements to AI System Controls

PCI DSS doesn't mention AI, but its requirements map directly onto AI system design choices. The table below summarizes the most relevant:

| Requirement | What It Covers | AI-Specific Implication |

|---|---|---|

| Req 3 | Protect stored account data | AI systems must not store raw PANs or CVVs; use tokenization |

| Req 4 | Protect data in transit | Prompt inputs and API calls to inference providers require strong cryptography |

| Req 7 | Restrict access by business need | AI agents need minimum permissions, scoped and time-limited |

| Req 8 | Identify and authenticate access | AI systems require unique credentials—not shared with humans or other systems |

| Req 10 | Log and monitor all access | Every AI inference, tool call, and agent handoff in the CDE must be logged |

| Req 12.8 | Manage third-party risk | AI vendors who process prompt data fall under service provider obligations |

Data Protection (Requirements 3 and 4)

The architectural answer to Requirement 3 is tokenization. When AI agents interact only with non-sensitive tokens rather than raw card data, the compliance surface shrinks and the risk of cardholder data appearing in AI outputs drops materially. The PCI SSC's tokenization guidelines confirm that properly implemented tokenization can reduce the number of system components requiring PCI DSS protection, though the tokenization system itself remains in scope.

Requirement 4 applies to every prompt sent to a cloud inference provider. Cardholder data transmitted to external AI APIs over unencrypted channels is a Requirement 4 violation. This includes prompt histories, context payloads, and debug logs: channels that compliance teams frequently overlook when scoping AI infrastructure.

Access Control and Least Privilege (Requirements 7 and 8)

AI systems must have their own unique credentials, not shared with human users or other systems, that can be tracked, rotated, and revoked. The PCI SSC AI Principles explicitly state that AI should be provided with limited, use-case-specific credentials.

PromptHalo implements this through agent security passports: signed credentials that travel with each agent request and contain embedded policy, budget limits, and authority decay parameters. Authority is scoped per action and enforced externally, so an agent cannot grant itself more access than it was issued.

Budget limits decay across time and steps, forcing re-authorization when thresholds are exceeded. This directly mirrors the least-privilege intent of Requirements 7 and 8.

Logging, Monitoring, and Incident Response (Requirements 10 and 12)

Requirement 10 demands that all access to CDE systems be logged. For AI, this means capturing not just final outputs but the full reasoning chain: prompt inputs, retrieved context, tool calls made, agent-to-agent handoffs, and outputs returned. AI's non-deterministic nature makes this especially critical, since the same input can produce different outputs, and models can drift over time.

PromptHalo's compliance-grade audit logs are append-only and tamper-evident, capturing every decision with its reason, acting agent identity, session context, and timestamp. Once written, entries cannot be modified or removed, creating the replayable evidence trail that QSA assessments and incident response require.

Three additional requirements extend directly into AI-specific scenarios:

- Req 12.10 (Incident Response): Plans must account for AI systems becoming attack vectors through prompt injection or model subversion, not just traditional breach paths.

- Req 11.6.1 (Script Integrity): Mandatory after March 31, 2025, this applies to AI-generated or AI-modified front-end payment page scripts.

- Req 6 (Code Review): Any AI-generated code deployed in the CDE requires security review before deployment.

PCI SSC's AI Principles: The Compliance Baseline

In September 2025, the PCI SSC published "AI Principles: Securing the Use of AI in Payment Environments"—the first authoritative official guidance on AI in PCI-regulated contexts.

The document uses a must be / should not be / should be / may be framework.

The single "must be" principle:

AI systems must be deployed and managed in compliance with applicable PCI SSC requirements.

Complexity does not exempt any requirement, regardless of how the AI system is architected or where it sits in the payment environment.

Key "should not be" principles for security teams:

- AI should not be trusted with high-impact secrets or unprotected sensitive data

- AI should not be given agency over operations requiring formal acceptance of responsibility—key custodian roles, management-level approvals

- AI should not be provided access to systems and information not required for its operation

Key "should be" principles that define good AI governance:

- AI should be logged and monitored so a responsible human individual can be held accountable for its actions

- AI should be validated prior to and throughout deployment—not just at launch

- AI should be protected against malicious input, including prompt injection and data poisoning

- AI should be implemented so it can be easily disabled if required

These principles don't introduce new requirements—they clarify how existing PCI DSS obligations apply to AI systems. For most organizations, the gap isn't awareness of these obligations; it's demonstrating that current AI deployments actually meet them, particularly around continuous monitoring, validated controls, and prompt injection defenses.

AI Governance Best Practices for PCI-Regulated Environments

Keep AI Out of Raw Cardholder Data

Tokenize before data reaches any AI system. Agents that interact with tokens rather than PANs or CVVs cannot expose what they don't have access to. This architecture contains PCI scope at the source—the AI system never handles regulated data directly, which simplifies technical controls and QSA conversations alike.

Single-use payment tokens or truncated PANs support AI-assisted payment workflows without exposing full PANs at the AI layer.

Implement Real-Time Input and Output Controls

Rule-based filters catch known patterns, but they miss novel prompt injection attempts, indirect RAG injection, and behavioral drift. ML-based detection at the inference layer closes that gap.

PromptHalo sits inline on every inference, tool call, and agent handoff, making per-action decisions in under 100ms—blocking prompt injection, jailbreaks, and data leakage before they execute. For each action, the system can allow, restrict, challenge, deny, or monitor, backed by an evidence trail. The platform achieves a 95%+ catch rate at under 5% false positives, compared to roughly 35% catch and 15–20% false positives for rule-based approaches. It deploys in under a day with no model retraining and no code rewrite.

Build Compliance-Grade Audit Trails

Every AI action in a PCI environment—every inference, tool call, and agent-to-agent handoff—must produce a tamper-evident, decision-level log. That means the full chain: inputs, retrieved context, actions taken, and the reasoning behind each decision, not just the final output.

These logs should be structured to support QSA assessments and map to specific PCI DSS requirements. Append-only storage ensures the record cannot be altered after the fact.

Treat AI Vendors as PCI Service Providers

Any third-party AI provider whose systems can access prompt data that may contain cardholder information falls under Requirement 12.8. This includes:

- Cloud inference providers receiving prompt payloads

- RAG platform vendors with access to document stores containing sensitive data

- Any vendor storing or processing AI interaction logs

Conduct due diligence, request Attestations of Compliance, and include explicit security obligations and incident notification requirements in vendor contracts. With third-party AI implementations accounting for 33% of financial services AI use cases, vendor risk is one of the largest unaddressed exposure points in PCI-regulated AI deployments.

Agentic AI and the Future of PCI DSS Compliance

McKinsey forecasts that AI agents could mediate $3 trillion to $5 trillion of global consumer commerce by 2030. That number suggests agentic commerce is not a future consideration—organizations building payment capabilities now are already building agentic ones.

What makes agentic AI categorically different from earlier AI in compliance terms:

- Autonomous tool calls that reach into payment infrastructure without human authorization at the moment of execution

- Multi-step decision chains where context and permissions accumulate across actions

- Agent-to-agent handoffs where trust and authority must be explicitly managed at each transition

- RAG retrieval pipelines that expand the attack surface to knowledge bases and external data sources

Traditional PCI DSS assumptions—discrete, human-operated system components with predictable data flows—don't map cleanly onto this architecture. The CDE boundary becomes genuinely difficult to maintain.

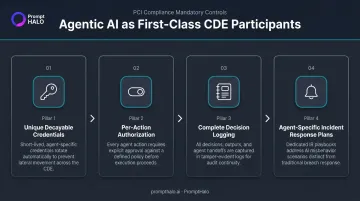

Organizations must treat AI agents as first-class CDE participants, not tools used by humans in the CDE. That means:

- Unique, decayable credentials per agent (not shared service accounts)

- Per-action authorization that doesn't assume prior context is still valid

- Complete logging of every agent decision, including handoffs between agents

- Incident response plans that account for agent subversion, not just system compromise

The PCI SSC's 2025 AI Principles publication signals that AI will receive more explicit attention in future standards versions — and that direction is only moving one way. Organizations that build AI governance infrastructure now, covering runtime controls, audit trails, vendor assessments, and human-in-the-loop checkpoints at high-stakes decision points, will absorb stricter future requirements without rebuilding from scratch.

Organizations that can demonstrate AI governance maturity ship agentic features faster. They already have the trust story regulators and customers require.

Frequently Asked Questions

Does using AI in payment systems automatically bring those systems into PCI DSS scope?

Not automatically, but the threshold is lower than most teams expect. Any AI system that stores, processes, transmits, or can impact the security of cardholder data is in scope—even without direct card number access. The "can impact security" clause is the key trigger, and it captures most AI systems integrated with payment infrastructure.

Which PCI DSS requirements are most directly affected by AI system deployments?

Requirements 3, 7, 8, and 10—covering stored data protection, access control, authentication, and logging—are the most immediately pressing. Requirements 6 (secure development and AI-generated code), 11 (penetration testing scope), and 12 (incident response and vendor management) apply directly to AI deployments in the CDE as well.

What is prompt injection, and why does it matter for PCI DSS compliance?

Prompt injection is an attack where malicious inputs override an AI system's instructions, causing it to extract sensitive data or take unauthorized actions. In a PCI environment, a successful attack can result in cardholder data exposure or fraudulent transactions—a direct compliance violation that existing network and endpoint controls cannot prevent.

Do AI vendors and LLM providers need to be treated as PCI service providers?

Yes. Any third-party AI provider whose systems can access or process cardholder information falls under Requirement 12.8 service provider obligations, requiring due diligence, compliance attestation, and contractual incident notification terms.

What is the safest way to use AI agents in a PCI-regulated payment environment?

Tokenize cardholder data before it reaches any AI system so agents work with non-sensitive tokens. Combine this with least-privilege credentialing (unique, scoped, decayable credentials per agent), real-time input and output controls at the inference layer, and complete audit logging of every agent action, including tool calls and handoffs.

How does agentic AI change an organization's PCI DSS compliance posture?

Agentic AI expands the CDE surface area by introducing autonomous multi-step actions, API calls, and agent-to-agent handoffs that blur traditional system boundaries. Organizations must treat AI agents as first-class CDE participants—with their own access controls, logging requirements, and dedicated incident response procedures—rather than passive tools operated by human users.